Nigeria Economic Update: Week Ended 24th November 2024

The Tinubu administration acknowledged that recent economic reforms have weakened Nigerians’ purchasing power but pledged to prioritize social investment programs to cushion the impact, maintaining a balance between reform and poverty alleviation. The IMF’s support for these reforms has boosted international confidence in Nigeria’s economic trajectory, potentially attracting more investors. As part of efforts to mitigate farmer-herder conflicts, strategic investments in the livestock sector are being implemented to improve agricultural opportunities and reduce socio-economic tensions.

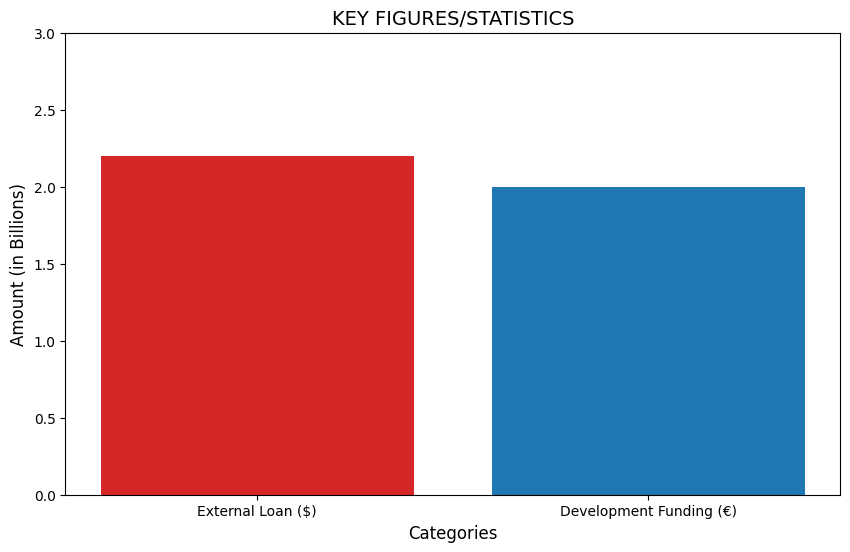

Also, government’s growing debt burden has been criticized and government has cautioned against the potential economic strain that will be caused by the recently approved $2.2 billion loan. On the infrastructure front, the Bank of Industry secured €2 billion to fund projects aimed at strengthening healthcare, energy, and food security, signalling the government’s commitment to development.